Liquidity is a powerful force that drives stock markets higher but doesn’t guarantee the upward trend over the long term. It is very difficult to even predict the timing of the reversal of liquidity. Should an investor thus take liquidity for granted knowing very well that the reversal of the trend is very difficult to predict?

The abundant liquidity channelized by QE (quantitative easing) by major central banks around the world since 2008 crisis has lifted prices across all the asset classes – Equity, Bonds and Real Estate and arrested the decline of Gold.

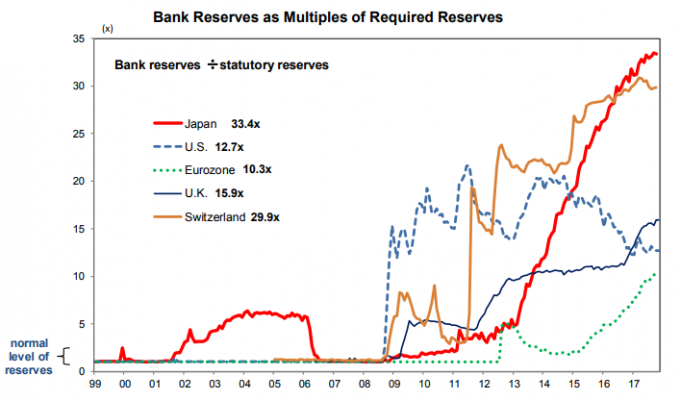

Source: Nomura Research Institute

Domestically, factors like demonetization, public awareness about mutual funds and TINA (there is no alternative) has resulted in a gush of liquidity in the stock market. The domestic liquidity is such that despite highest selling by FIIs after 2008, markets have only risen. But now the sands are shifting.

Case in point is the recent sharp decline in mid & small cap stocks which wiped out entire gains since Sep 2017 in Nifty Mid Cap Index and June 2017 in Nifty Small Cap Index. As been the case historically, many people were caught off guard by this correction. The sharp decline was expected in this space as the valuations crossed the levels never seen historically. The downside risk is excessive for higher priced assets while future potential returns are low over the long term.

Truemind has stayed away from Mid & Small Cap since last 1 year on the back of high prices. We also exited from this space in a gradual manner. Truemind believes that there is more pain left in mid & small cap space.

Another case in point is the falling bond prices and rising yields. Many in the markets expected interest rates to go down or continue to stay lower anchored by their recent experience. However, we believed that the interest rate cycle has bottomed and is on the path of an uptrend. Very visible reasons were the reversal of QE (quantitative easing) to QT (quantitative tightening) by the USA, impact of GST, an uptrend in global crude oil prices and fiscal deficit constraints. Thus we were very careful in parking the funds meant for safer investments in low maturity portfolios of debt funds. This ensured lower mark to market impact on portfolio values. Recently, many banks have raised their deposit rates. Truemind expect that interest rates will be hardened further this year.

US initiated QT plan to suck out USD 2 trillion from the FED Balance sheet with debt of USD 4.5 trillion. Many market participants in our view are underestimating the potential of such loss of liquidity. As QE helped inflate asset prices, reversal of the same would deflate asset prices. This would be more visible when other developed economies like Europe, UK & Japan would also start their version of QT, sooner or later.

FED Quantitative Tightening (QT) Schedule

Source: Nomura Research Institute

The markets are currently at crossroads. Domestically, on one hand, we have positives like improving economic growth, higher earnings growth, election-related spending and fast-tracking of Govt. projects before the general elections. On the other hand, the impact of QT, rising interest rates, higher CAD and its impact on the exchange rates and election uncertainties would result in higher market volatility.

We are hoping that this ensuing volatility would offer opportunities to invest at reasonable market levels. At 23x PE of Sensex, Indian markets are one of the most expensive markets in the world. Historically, no one has made decent long-term returns by investing at higher valuations, though short-term returns may give a different impression. Therefore, for generating higher long-term returns on investments, one has to wait for right opportunities and be content with lower returns in the short term. Short term pain would lead to getting long-term gains.

Truemind investment strategy continues to take cautious approach towards Equity due to excessive valuations. Some pocket of attractive valuations in IT last year has given good returns in our investment portfolio and now it appears to be fairly priced. Large Cap pharma stocks appear to be attractively priced and one may take the position in those stocks with 3 to 5 years of time horizon. Gold as a portfolio hedge and a safe haven in time of uncertainties should be 5-10% of an overall portfolio. Especially, at the time when the Gold asset has not performed well over the last 4-5 years. Higher debt yields, after a recent spike, provide good opportunities to earn higher post-tax returns for investments meant for FDs. However, the debt portfolios should be carefully selected based on their holdings, YTM (yield to maturity) net of expenses and portfolio maturity.

2 Comments

Pingback: What Is Causing Market Panic And How To Deal With It | Investment Blog

Pingback: Is it a Structural or Cyclical Correction? - Investment Blog