When Sharma Ji ka ladka gets a job with a decent salary, he is urged by his parents to buy a house as soon as possible on loan and pay EMIs. There is a traditional mindset of having own house which percolates from parents to their young generation. What was right in old days is not right today when everything about lifestyle has changed so drastically. Buying a house early in your career is not correct based on not just economical aspect but the convenience and better lifestyle aspect as well. Let’s take it one by one.

Convenience Aspect:

In a fast-changing world and rising aspirations, we seek better jobs with good pay and work satisfaction. Thus switching jobs is quite common. Also, there are sudden rise and fall of one’s requirement and growth prospects in an organization with falling levels of job security that can lead to changing companies.

Imagine a situation where you have bought a house near your work location, and one fine day you get an offer to work in your dream company or desirable work profile in another city. Will you leave that offer just because you are stuck with a house? I am sure you would not like that chance to slip away. The alternative would be to rent your current house and take on rent another apartment closer to your new office. Although sounds easy, it is very difficult to manage your tenants and maintenance of your own house when not in the same city.

Another undesirable aspect of buying a house on EMIs is giving up your freedom to let go. You cannot let go your monthly salary to start any venture of your own. You cannot let go job income even if your boss has made your life a hell. You start sweating on any prospect that could affect the safety of your job. Thus living in a burden of worries till the sword of EMI is hanging on your head. Would you like to live prime years of your life in constant fear and worry leading to loss of sleep and hair?

Better Lifestyle Aspect:

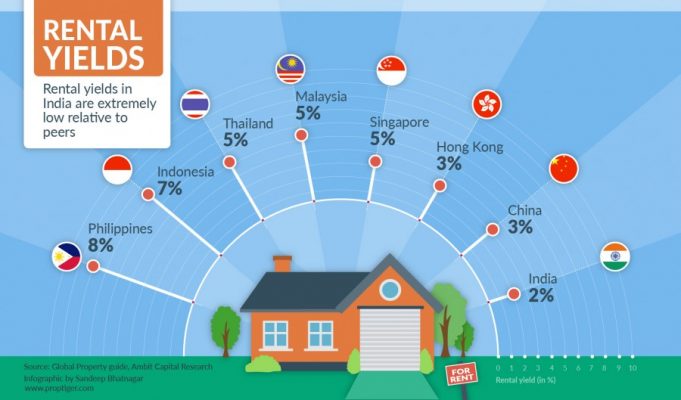

Many people do not know that one can stay in a great locality/society by paying rent which is much lower than paying for EMIs for a home in a mediocre society. This is possible because rental yield in India is on an average 3% based on analysis by Magicbricks. That means you pay on an average INR 3 lakhs per annum (or INR 25,000 per month) as rent for a property worth INR 1 crore. Whereas for the same property if owned (assuming 100% on loan for fair comparison), you pay EMI of whopping INR 10.80 lakhs per annum (or INR 89.97 thousand per month) for 20 years at 9% home loan rate. You are thus paying roughly INR 8 lakhs more in EMIs, to begin with.

Thus to reduce your EMI outgo, you will have to compromise with mediocre society to own a home. The mediocre society may not have desired lush green lawns, clubs or facilities for you and your children. This would also mean the cut down on dining outside, buying a new dress and vacationing on foreign locations.

Economical Aspect:

Last but the most important aspect for not purchasing a home early in your career is the economical aspect.

Thanks to the huge mismatch in rental yields (~3%) and home loan rates (~9%) in India, it makes great economic sense to stay on rent till closer to retirement and invest in higher yielding asset class for your dream home. Why closer to retirement? Because you are in a much better position to decide the best place to spend rest of your life. Fast changing face of cities and towns with localized problems of pollution or water scarcity would guide a better decision to own a home post-retirement.

Let us see how the math work out when you purchase a home on EMIs or when you stay on rent and invest in equity mutual funds via SIP mode. Historically, equity mutual funds have appreciated at a much faster pace compared to real estate prices in the long term.

Assuming the first scenario when you purchase a home of worth INR 1 crores bought on EMI for 20 years. We are not assuming any down payment for a fair comparison. Below are the statistics:

You pay net total amount of INR 2.05 crores in EMIs over the period of 20 years. We are not even accounting for cost associated with maintenance of home.

Now, assuming the second scenario when you stay at a rented accommodation. Below are the statistics:

You pay roughly INR 99.19 Lakhs (assuming 5% escalation on rent every year) over 20 years on rent for a property worth INR 1 Crore at present.

Further, you invest the difference between rent and EMI in equity mutual funds for 20 years.

By investing about INR 1.17 Crores, your investment value is worth astonishing INR 5.06 crores after 20 years on 12% expected returns. Historically, mutual funds SIPs have delivered ~15% returns over the period of 10-15 years.

The house which is worth INR 1 Crores now would be worth INR 2.65 Crores on the back of 5% expected annual appreciation over 20 years.

That means, you not just own a house by paying fully but also have saved some surplus for your retirement fund! Isn’t it amazing? Even if you assume a higher rate of appreciation in rent/house property, you still end up with some surplus.

This is possible due to the high gap between rental yield and home loan rates in India plus higher returns from equity mutual funds. In developed economies, the difference between rental yield and home loan rate is minuscule. The only scenario it would make economic sense to purchase a home on EMI is when the difference between rental yield and home loan rate has narrowed down to 2-3% over the long term from ~6-7% at present.

We hope you are now in a position to understand cost & benefit in purchasing a house versus staying on rent and investing the difference in equity mutual funds. This should surely help you make a more informed decision for a better life.

3 Comments

Good insight. Hope to convince our parents for not buying a property this early.

I was convinced till the paragraph where some terms related to “Rental Yield” was used.

So are we saying when this difference will reduce then its good to buy a home of your own ?

Yes, your understanding is correct. In developed economies, the difference in rental yield and home loan rates is minimal. However, in a growing economy like India, a difference of not more than 4% should be acceptable. When this scenario emerges, it would be a good time to invest in real estate.