At Truemind Capital, our broad understanding has been:

- The current environment calls for diversification across asset classes and geographies, as global uncertainties continue to shape market outcomes.

- Investments should be guided by valuations and margin of safety, ensuring downside risks remain contained rather than chasing expensive opportunities.

- Asset allocation needs to be dynamic, with active rebalancing across asset classes as valuations and opportunities evolve.

- Maintaining liquidity within portfolios remains critical, enabling timely shifts and effective deployment during market dislocations.

Equity Market Insights:

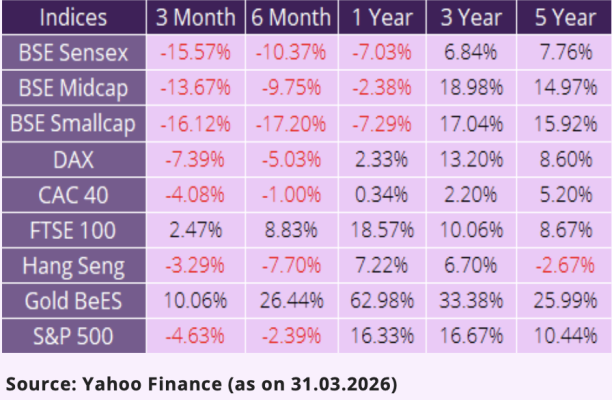

Indian equity markets remained under pressure during the January-March 2026 quarter, marking a weak close to the financial year. Benchmark indices ended FY26 in negative territory, with the BSE Sensex declining around 7% year-on-year, reflecting a broad-based moderation after the strong gains seen in previous years.

Market performance during the quarter remained uneven. While large-cap indices showed relative resilience, broader markets continued to lag, with mid- and small-cap segments witnessing pressure amid stretched valuations and moderating earnings expectations. Participation remained selective, with returns concentrated in limited pockets rather than being broad-based.

The ‘Oil & War’ Punch: Market sentiment turned sour in February as the West Asia conflict flared up. We saw Brent crude spike from $72 to over $100 within weeks. Escalating geopolitical tensions and a sharp rise in global uncertainty have raised concerns about inflation, currency stability, and interest rates in the home turf. This, in turn, weighed on investor confidence and led to increased volatility across equity markets.

Foreign institutional investors’ (FIIs) flows also weighed on this cautious environment. FY26 saw one of the highest levels of foreign outflows, with March alone witnessing outflows of over Rs 1.14 lakh crore (around $12.3 billion) from domestic equities. Domestic institutional investors, however, continued to provide strong support, partially offsetting the impact of global risk aversion.

Globally, economic growth remains below its long-term average due to persistent geopolitical tensions and trade-related uncertainty. Markets appear to be entering a late-cycle phase, where returns are likely to be more uneven and increasingly selective. While liquidity conditions remain supportive, the effectiveness of liquidity in driving market returns is gradually diminishing.

Looking ahead, corporate earnings growth is expected to remain moderate and uneven. We are seeing a clear ‘late-cycle’ shift. While companies may still grow their top lines (revenues), the bottom line (profits) is being squeezed by rising costs and limited margin expansion.

Valuations, while corrected from their peaks, are hovering above long-term averages, particularly in the broader market segments. While the recent correction has improved relative valuations compared to emerging markets, this does not necessarily translate into immediate upside, especially in the absence of strong earnings momentum.

In addition, elevated fiscal deficits across major economies, ongoing geopolitical developments, and policy uncertainties continue to complicate the global investment environment. In such conditions, strong macro data alone may not translate into broad-based market performance.

What we are doing?

Against this backdrop, we continue to actively rebalance portfolios during periods of volatility, using short-term debt allocations as a source of liquidity to deploy into equities at more reasonable valuations. This allows us to maintain alignment with client risk profiles while tactically adjusting exposure as opportunities emerge.

We continue to choose portfolios tilted towards large-cap and value-oriented strategies, complemented by selective global exposure for diversification, while avoiding aggressive thematic and momentum-driven allocations.

We believe equity returns over the medium term are likely to be more moderate and earnings-driven, making disciplined portfolio construction more important than chasing short-term market trends.

Debt Market Insights:

Debt markets also remained under pressure during this quarter, with yields moving higher across the curve, particularly at the long end. This shift was driven by a combination of global and domestic factors, including elevated crude oil prices and expectations around inflation.

This has been reflected in government bond markets, where the 10-year G-sec yield moved closer to the 7% level, approaching its highest levels in nearly two years. Rising oil prices and currency pressures further added to inflationary concerns, while elevated bond supply also contributed to upward pressure on yields.

From a policy standpoint, the Reserve Bank of India maintained a neutral stance, keeping the repo rate unchanged at 5.25% and has revised its GDP estimates marginally downward for Q1/Q2FY27 to 6.8% and 6.7%, respectively. In our view, the current rate environment suggests limited room for further rate cuts in the near term. The trajectory of interest rates will largely depend on how inflation evolves, particularly in light of sustained energy price pressures, and the extent to which growth is impacted over the coming quarters.

As yields have moved higher, bond prices have adjusted accordingly, leading to mark-to-market pressure, particularly in longer-duration instruments. This dynamic has been visible across debt mutual fund categories, where longer-duration funds have seen more volatility compared to shorter-duration segments.

At the same time, the rise in yields has improved the overall carry available in fixed-income markets. With yields at relatively higher levels, investors are able to lock in more attractive accrual opportunities, particularly in shorter-duration instruments.

Our Approach to Debt Allocation

At Truemind, we continue to view debt as a stabilising component of portfolios rather than a source of return maximisation. Given the current environment, we maintain our preference for shorter-duration and high-quality accrual strategies, where the risk-reward profile remains more favourable. These segments offer better visibility of returns while limiting exposure to interest rate volatility as compared to longer-duration exposures.

We also continue to utilise arbitrage funds and short-term debt instruments as part of portfolio construction, particularly for managing liquidity and enhancing post-tax efficiency.

As the interest rate cycle evolves, opportunities in duration may emerge. However, at present, maintaining a disciplined and selective approach remains key to navigating the fixed income investments.

Other Asset Classes:

Gold too witnessed a volatile phase during the recent period, with prices moving in both directions rather than following a clear upward trend. While global uncertainties and geopolitical tensions typically support gold prices, the recent period saw intermittent corrections driven by profit booking and liquidity needs.

That said, gold continues to play an important role as a portfolio diversifier, particularly in periods of elevated global uncertainty. However, its short-term movements may remain influenced by a combination of factors, including global liquidity, currency movements, and investor positioning.

The real estate sector continues to show a mixed trend. While residential prices have remained firm, particularly in premium segments, demand has been increasingly selective across markets.

Recent data shows moderation in activity, wherein housing sales declined on a quarter-on-quarter basis amid global uncertainties, even as long-term demand remains resilient. Growth continues to be concentrated in higher-ticket segments, while affordability constraints and cautious sentiment have weighed on broader participation. Given its cyclical nature, illiquidity, and evolving demand dynamics, real estate should be viewed as a complementary asset within a well-diversified portfolio.

Truemind’s Model Portfolio – Current Asset Allocation

Personal Finance Capsule:

Investment Impact of War

How to survive your finances in Global uncertainty?

For any query or discussion, you can get in touch here: https://www.truemindcapital.com/contact-us