At Truemind Capital, our broad understanding has been:

- Diversification across asset classes, sectors and geographies remains the best defence in a world where market narratives can change quickly.

- Wealth preservation takes precedence over chasing returns. Investment decisions should continue to be guided by valuations and margin of safety rather than market momentum.

- Asset allocation needs to remain dynamic, with portfolios actively rebalanced as opportunities and risks evolve.

- Maintaining liquidity within portfolios remains critical, enabling timely shifts and effective deployment during market dislocations.

Equity Market Insights:

The April-June 2026 quarter was dominated by geopolitical uncertainty. What had been simmering for months escalated as the Israel-Iran conflict widened, with the US joining Israel in strikes on Iranian nuclear facilities and hostilities spilling over into Lebanon. The resulting surge in crude oil prices revived concerns around inflation, interest rates and global growth. By late June, however, tensions had begun to ease. A ceasefire and signs of renewed US-Iran peace talks pulled Brent crude down from above US$92 per barrel to around US$73 as shipping through the Strait of Hormuz gradually resumed. This eased pressure on India’s import bill, the rupee, and inflation expectations, helping domestic equities recover some lost ground towards the end of the quarter.

Indian markets have largely been range-bound during the quarter, only normalising after hopes for peace talks emerged in late June. The BSE Sensex and Nifty 50 gained around 6-7% each over the April-June quarter, but both indices remain down close to 9-10% on a calendar year-to-date basis, reflecting the scale of the correction amid global risk aversion and geopolitical uncertainty. FPIs remained persistent sellers throughout the quarter, pushing total outflows from Indian equities past Rs 2.7 lakh crore in 2026 – already exceeding the entire outflow recorded in 2025.

As companies begin reporting their April-June quarter results, revenues are expected to remain healthy despite the challenging operating environment. Crisil Intelligence estimates India Inc.’s revenue grew 11-11.5% year-on-year in Q1 FY27, while operating margins may contract by 75-100 basis points owing to higher fuel, freight and raw material costs arising from the West Asia conflict. While Geopolitical tensions may ebb and flow, the impact of such elevated input costs would likely reflect in corporate profitability with a lag, keeping margin pressures intact over the next few quarters.

Globally, US markets once again showed how quickly investment narratives evolve. While technology stocks recovered towards the end of the quarter as geopolitical tensions eased, market leadership broadened beyond the handful of mega-cap AI companies that had dominated returns over the past few years. Smaller-cap companies and traditional sectors such as industrials, transportation, and financials outperformed many of the market’s best-known technology names, reminding investors that concentrated themes rarely lead markets indefinitely.

For us, this reinforces an important investment principle. Markets will always find a new narrative, whether it is artificial intelligence, energy, or another emerging theme. Long-term wealth creation, however, comes from disciplined portfolio construction, sensible valuations, and diversification rather than concentrated bets on the market’s latest favourite.

What we are doing?

We continue to maintain equity allocations in the 30-60% range (based on individual risk profiles), with portfolios tilted towards large-cap, value-oriented portfolios diversified across sectors and geographies.

While valuations remain elevated across several markets, we believe patience and discipline are more important than chasing momentum-driven opportunities. Maintaining liquidity and actively reviewing portfolios allows us to deploy capital as more attractive opportunities emerge, while keeping portfolios aligned with long-term objectives.

Debt Market Insights:

In the recent past, the Indian bond market has faced an unusual challenge. Normally, when inflation is under control and the RBI cuts interest rates, bond yields tend to fall. However, this time, bond yields remained elevated.

Why did this happen?

The biggest reason was global capital flows. Investors were attracted to opportunities outside India, particularly:

- Higher interest rates in the US,

- Geopolitical uncertainty arising from the conflict in West Asia, and

- The global excitement around Artificial Intelligence (AI)-related investments.

As a result, less foreign capital flowed into India, putting pressure on the rupee and keeping domestic bond yields higher than expected.

The Apr-June 2026 quarter witnessed a tumultuous period that saw the most significant volatility since the pandemic. Fortunately, two important developments provided relief to the markets.

First, the Government of India and the RBI have introduced measures to attract more foreign capital. These include incentives such as the FCNR deposit scheme and tax exemptions for foreign investors investing in government bonds. These steps have already started improving foreign investment into Indian debt markets and have eased concerns around funding and currency stability.

Second, the easing of tensions in West Asia has led to a sharp correction in crude oil prices.

What Does This Mean for Interest Rates?

We believe the recent developments reduce the likelihood of any immediate increase in interest rates and possibly a 25-50 bps rate hike towards the second half of the financial year. Global developments remain key. Renewed geopolitical tensions in West Asia and any delay in easing global inflation could influence the RBI’s stance. Equally important will be the US Federal Reserve’s rate cycle. If the Fed keeps rates higher for longer, the RBI may have to respond to support the rupee. Significant rupee depreciation remains a “massive concern” for foreign portfolio investors, as it can erode the inflation-adjusted returns of Indian assets compared to risk-free US yields.

Going forward, currency stability and global interest rates will continue to be important drivers of India’s bond market outlook.

Our Approach to Debt Allocation

At Truemind, we have consciously avoided taking aggressive duration calls over the past two to three years. In a world characterised by inflation uncertainty, geopolitical conflicts and volatile global interest rates, we believed that the risks associated with long-duration bonds outweighed the potential rewards.

Even today, we continue to favour a balanced approach by maintaining exposure towards shorter and intermediate-duration debt instruments that offer an attractive combination of yield, liquidity and lower mark-to-market risk. The 10-year G-Sec yield is currently around 6.70%–6.75%, and one-year CDs are offering yields near 6.90%, which is considered a decent carry in the current liquidity environment.

We believe debt should play a much larger role than simply generating returns. It acts as the stabilising anchor of a portfolio, providing regular income, preserving capital during uncertain periods and creating the flexibility to rebalance into equities whenever markets present attractive opportunities.

Other Asset Classes:

Gold: After a strong rally over the past two years, gold underwent a healthy correction during the quarter, ending June around US$4,000/oz as safe-haven demand eased and higher interest rate expectations weighed on prices. Even so, the long-term case for gold remains intact. We continue to view gold as a strategic portfolio diversifier, supported by central bank buying, de-dollarisation and its ability to provide resilience during periods of uncertainty.

Real Estate: Housing sales across India’s top 7 cities fell about 6% YoY in the April-June quarter, with new launches up 7% YoY and average prices rising a modest 7% annually, a clear moderation from last year’s double-digit pace, as per Anarock data. We continue to view real estate as a complementary, not core, allocation given its illiquidity, cyclical nature, and relatively high transaction costs.

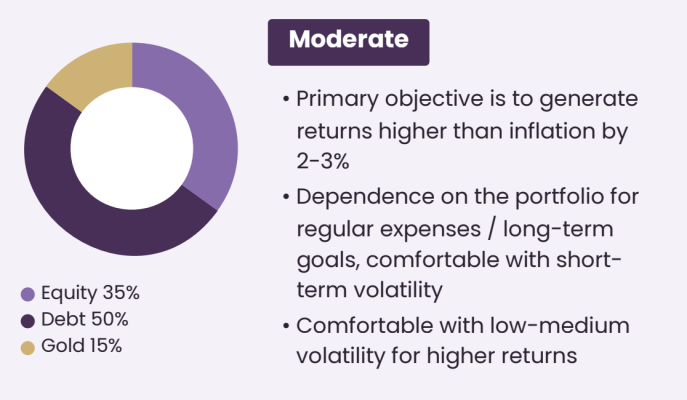

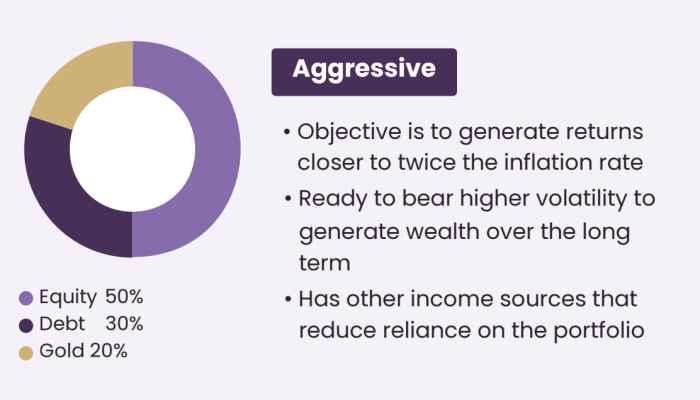

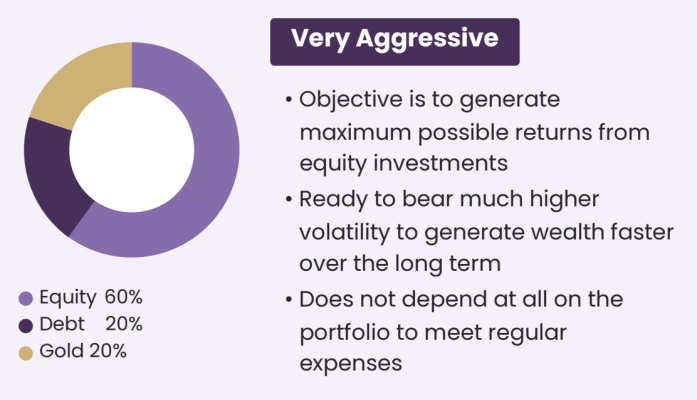

Truemind’s Model Portfolio – Current Asset Allocation

Personal Finance Capsule:

Realign your portfolio before it’s too late

At Truemind Capital, we help people achieve peace of mind by managing their financial planning and investments in India and globally diversified portfolios.

For an introductory call, reach out to us at: https://www.truemindcapital.com/contact-us