Sensex has declined by 12% from its all-time high of 38,989. BSE Mid Cap Index and BSE Small Cap Index are down by 24% & 31% respectively from its peak level. Many people who get carried away in the bullish market sentiments turned speculators and are now feeling the pain. In this communiqué, we are going to discuss the reasons for the market fall and investment strategy to deal with the current situation.

Following are the biggest reasons for the market decline (not in a particular order of its importance to the Indian economy)

Global Crude Oil: Global crude oil prices have risen sharply (54% YoY) over the last one year – London Brent Crude Oil is trading at $86/barrel now vs. $56/barrel a year ago. The steep rise in prices came on the back of higher demand projection for oil and increasing supply constraints – US sanction on Iran, lower than expected output from Shale gas etc. In our view, this is the biggest factor for anxiety in the Indian stock market.

Source: www.macrotrends.net

Since India imports 80% of its oil requirement, the higher crude prices put a significant burden on the country’s finances. The stretching of the current account deficit (exports minus imports) leads to a higher demand for USD vs. INR that result in depreciation of the local currency. A weaker currency further compounds the import cost of crude and all other imported goods.

Consequently, the imported inflation leads to increase in prices of everything from food grains to consumer durables to basic goods as transportation cost and raw material cost goes up. Many companies, especially in the mid and small cap space would see margin erosion on higher raw material cost and declining demand due to increase in prices across the board. This dual attack would impact the top-line and bottom-line.

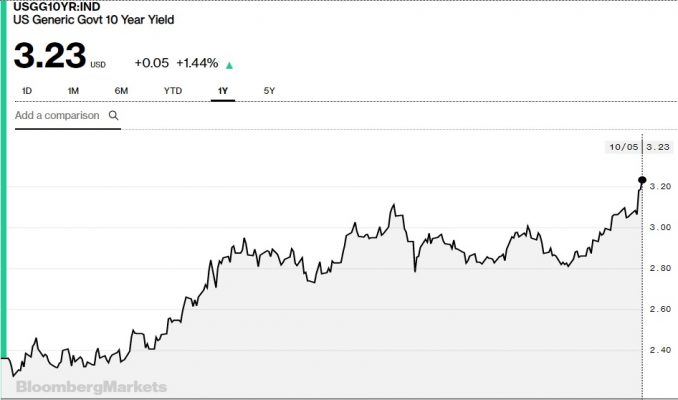

Increasing Interest Rates: With rising inflation comes higher interest rate. Central banks around the world have been turning their focus from quantitative easing (QE) to quantitative tightening (QT) after multiple years of easy liquidity.

FED in the US has raised interest rates three times and expected to increase one more time this calendar year. The key reasons are the improvement in US economic growth rate, multi-decadal low unemployment rate and increase in the core inflation. There is also an understanding among FED officials that they need to bring normalcy in interest rates and reduce the balance sheet debt in order to be prepared (with tools) for the next recession.

Source: www.bloomberg.com

European Central Bank (ECB) has also reduced its bond-buying program and plans to completely stop it in the next few months. Japan although has not made an official announcement but they have also started taking minor steps for reducing the size of its balance sheet.

We reasoned in our earlier blog about the expected rise in interest rates and its potential impact on the global economy. The rise in the domestic interest rates was expected on the back of major central banks turning to QT, which leads to rise in global interest rates; uptrend in crude oil prices; waning of liquidity after demonetization with the return to normalcy; and the impact of GST (though largely controlled by the Govt.).

Increasing interest rates have exposed the fragility in the Indian financial system with default fear by IL&FS and asset-liability mismatch problems in other banks and NBFCs. When there is an abundant liquidity in the system, many a time risk management measures are relaxed leading to problems when situation reverses to tighter liquidity. We are afraid that the stability in the Global economy built on years of easy liquidity could be threatened due to QT. If our fear comes true, we may see a catastrophe in equity markets around the globe.

Trade Wars: The US initiated tariffs on Chinese, European and other country’s goods have added another reason to worry. China responded with counter-tariffs on US goods, so did European nations. Any further escalation would affect the transaction and trading eco-system around the world.

This could lead to full-blown trade wars where the reverse of global free trade would impact all the economies around the world. We, however, hope that some sanity would prevail in the US legislators that would prevent from any such scenario to emerge amid weakness across European and emerging market economies.

Election Related Uncertainties: Over the next 8 months, we are going to witness important state elections – Rajasthan, Madhya Pradesh and Chhattisgarh; and general elections in May 2019. NDA led by PM Narendra Modi has been the current favorite for the Indian investment community. The market is pricing in the re-election of NaMo as PM for continuity of reforms. As we are approaching closer to elections, there is an increasing feeling in the market that the re-appointment of NaMo as PM would not be easy on the back rising anti-incumbency and opposition unity.

This would further dampen sentiments leading to erosion of NaMo premium in the equity market prices. Already, it appears that BJP is on a sticky wicket in upcoming state elections. If the results confirm the same, we can expect a further decline in market sentiments.

Investment Strategy:

Truemind Capital has remained consistent with its investment philosophy which was established on the principles of mean reversion and value investing. We have been underweight on equity since last 6-9 months (equity exposure ranging from 20% to 45% in Large Cap equity schemes) in our client’s portfolio on the back of steep valuations. We exited completely from mid & small-cap portfolios by April this year. Some other successful calls were exposure to information technology funds last year and investment in lower duration debt funds.

Despite recent corrections, we still believe that valuations are not comfortable enough for lump-sum investment in equity mutual funds. SIPs and STPs should be continued to take advantage of market volatility over medium to long term. On a relative valuation basis, large-cap value portfolios are still better placed than mid and small-cap schemes. Any further weakness of 12%-15% in the market would be a good time to start taking higher exposure to equity mutual funds with an emphasis on portfolios which are following value investment strategy. We believe that such opportunities have a high probability to arise over the next 6-9 months due to above-mentioned reasons. A sharp decline in global crude oil prices can, however, reverse the negative sentiments.

On the debt side, interest rates are expected to further firm up. However, we believe short to medium term debt portfolios offer good opportunity to invest at higher yields. However, portfolio quality and risk management processes are of utmost importance for scheme selection.

To end this article, we re-iterate that risk is in the price at which one buys an asset. With the margin of safety principle (value investing) in mind, one can reduce the downside risk while enhancing the upside potential. However, to be able to stick to this philosophy amid market noises, one needs patience, time and courage. These qualities have always ensured long-term investment success.

6 Comments

Very thoughtful and well written

Thanks for the feedback 🙂

Exposure in nbfc which deals with short term lending like in consumable goods would be strategic investment.

Agreed with your thought process of SIP/STP Route to invest in market and building up majorly around Large cap names…..just one thing want to understand from article ……..If Other than NDA Comes then is reforms stop ?

Here i not fully agreed and believe main task of MODI/NDA is to tatget reform and forced other parties also consider development and reform as major agenda for their election so whichever Govt comes in power they have to fear if they still confined to caste based politics and not development as main agenda then have to ready for public anger as well…..

Rest For investments better times are coming and one keep evaluate themes and names as some serious investment opportunities started shaping up and will see more such opportunities to emerge ….just need courage and patience to encash the same.

There may not be a discontinuity in the reforms, irrespective of the party in power. It is just that market has been giving a good premium to NaMo led NDA govt. The market has its own way of thinking 🙂

Pingback: Market Cycles & Investment Lessons from History | Investment Blog