As I am writing this piece, I am sure many are already aware of the issues impacting the global economy – a global slowdown, trade wars, and burgeoning debt; and issues affecting the domestic economy – falling consumption, NBFC led confidence/liquidity crisis and constrained fiscal space. Many, however, are unable to understand if these issues are short term in nature or the long term. In other words, whether it is just a short cyclical correction that will see a quick recovery or it is a deeper correction which is structural in nature that would take a few years to recover. Although, you probably have heard arguments for both the correction possibilities – cyclical and structural, we are sharing our thoughts on the same and how we can position the portfolio to take advantage of whatever the scenario we come across.

Let’s first look at the global scenario. More than a decade ago, the subprime crisis emerged due to the lax regulatory environment, benign credit rating agencies and higher level of debt. Many countries were essentially living beyond their means for decades. The response to solve the issue by all the central banks and policy-makers around the world was an even higher level of debt. Some tweaks in regulation and risk measures were surely made but more focus had been on pumping the world with cheap money through Quantitative Easing (QE).

Unprecedented liquidity levels further inflated the prices across all the asset classes – Equity, Debt, Real Estate and now Gold – a rare phenomenon. Instead of world correcting the habits of living beyond means, easy liquidity further invigorated the animal spirit to such an extent that absurdity started appearing normal. We have been seeing a rising level of debt trading at a negative yield – a staggering $16 trillion now! We first highlighted the risk of rising levels of bonds with a negative yield in our blog written in June this year. Some wonder, why anyone would purchase a negative-yielding bond – well simply to sell it to a bigger fool at higher price; fundamentals can take a back seat.

Other absurdities can be observed in the valuations of startups. A good piece written by an NYU’s professor on WeWork recently is an apt case in point. The irrationality all around indicates that people are making decisions after getting heavily sedated by the addiction of easy money, backed by the major central banks’ assurance of doing ‘whatever it takes’.

The size of the US corporate bond market rated BBB (a notch above junk) has never been bigger. A substantial amount of private debt is backed by loans against shares globally (similar case in India). A fall in equity can result in lenders rushing to sell equities further to recover their debt which could lead to a catastrophic drop in equity valuations throwing the world into depression & chaos instantly. Probably this explains why central banks are so sensitive about the decline in equity prices. US FED which was talking about increasing the interest rates and carrying Quantitative Tightening (QT) till the beginning of the current calendar year; made a classic u-turn (they will do QE instead of QT) when S&P declined from 2900 to 2300 within 2-3 months.

In short, globally, the structural issues which created the problems at the first place weren’t addressed; rather the can was kicked down the road and magnitude of the problem was increased. Surprisingly, the answer to these issues continues to remain the same – more QE!

Now let’s look at the domestic scenario. India had always remained relatively resilient to global shocks due to strong internal consumption on the back of high savings rate and young demography. Not anymore. It seems we have taken the demography and savings factors for granted for far too long. Twin blow from demonetization and poor implementation of GST reforms has crippled the informal sector having strong linkages with the formal economy. Not focusing enough on education and healthcare has produced many youngsters joining the workforce with lower skillset/talent to be considered for quality jobs (which pay well) that affect new demand. This also poses challenges to our long term growth prospects.

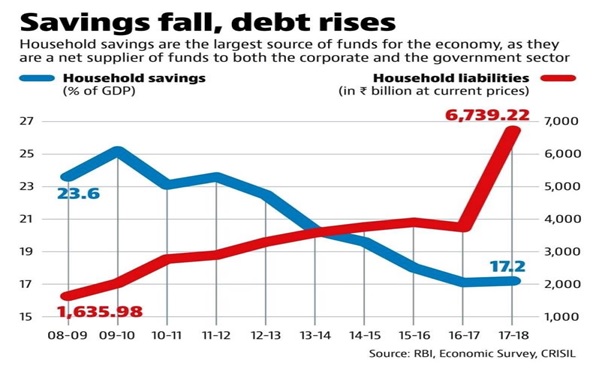

Savings, which have financed consumption and investments, have been declining steadily over the last decade. Many lakhs of crores of investments are stuck in unfinished real estate projects rendering the investments completely unproductive which affected the velocity of money that fuels GDP growth.

In good times, the sectors which were avoided by the banks were funded through the NBFC route. The proportion has become big enough that it cannot be quickly resolved in an environment where PSU banks are also burdened with gigantic NPAs. Creation of IBC is a great step to resolve this mess but the resolution pace has been painfully slow. Watch-out for the NBFC led crisis engulfing the real estate sector after the auto industry.

India’s economic fundamentals have weakened over the last decade. Unlike the last time during the global recession in 2007-08, we do not have enough fiscal space to provide stimulus. Our fiscal deficit is much higher than the officially reported figure of 3.40%. Based on the calculations of CAG, if we account for all the off-balance sheet debt of the Central Govt., the fiscal deficit is more than 5.5%. (https://www.moneycontrol.com/news/business/economy/cag-pegs-indias-fy18-fiscal-deficit-at-5-85-vs-govts-3-46-report-4243791.html)

This is the precise reason that the Govt. is desperately eying the RBI reserves and trying to sell PSU assets. For disinvestment also to take place, market sentiments need to be good or else we have our savings at risk. (https://theprint.in/economy/modi-govt-risks-national-small-savings-fund-by-using-it-to-support-struggling-psus/278698/)

After recent stimulus announcements, the market is awaiting more action from the Indian Govt. in the form of an effective and substantial stimulus package. However, as I have mentioned above, the capacity to provide big stimulus is limited. The recent announcement of RBI transferring surplus money has been a big booster shot in the arm of the Govt. that will help it meet the fiscal deficit targets amid dwindling tax revenue growth. How the Govt. allocates this fund would be a major factor that will decide its impact to kick start the economic growth. If done right, we may see a softer landing amid chaotic global environment.

Considering both the global and domestic scenarios, it appears we are in a situation which has no quick fixes. The correction is more structural than cyclical in nature. The way we witnessed fast recovery in 2008-09 on the back of stimulus may not be witnessed this time. We will surely have a recovery but in how many years is anybody’s guess. So how should we position our portfolio for an uncertain time? The key is ‘tactical’ asset allocation, a must in all market scenarios to generate above-average returns in the long term. Importance of ‘tactical’ asset allocation (that justifies 80% of portfolio returns) has further increased due to a highly dynamic and competitive investment scenario.

First of all, one needs to be very clear of her risk profile and decide a range of equity allocation on that basis. For example, a moderate risk profile should decide an equity allocation range of 20-60% and rest in debt. At fair market valuations, equity allocation should be around 40%. One should move to a lower level of 20% gradually when market prices start moving above the underlying fair value and sentiments cycle is marching towards its peak. During this journey, the downside risk is increasing whereas upside potential is limiting.

Similarly, one should start increasing the allocation gradually to 60% when the sentiment cycle is sliding towards the trough. At the lower end of the sentiment cycle, the downside risk is limited and the upside potential is higher. To read more about the sentiment cycle, click here. If you haven’t applied an appropriate asset allocation to your portfolio yet, do it now and don’t get bothered by the sunk cost fallacy.

Following this investment strategy (buying low & selling high) would ensure lower downside and higher upside potential. The strategy is logical and easy to understand but very difficult to implement due to sophisticated skill-set required for asset allocation calls (across asset classes, sub-categories, and schemes), evaluating the fair market value, understanding the phase of sentiment cycle and keeping the emotions under check. The whole exercise requires a lot of patience.

The tactical asset allocation strategies have worked well for us at Truemind Capital. As guided by our investment philosophy, we have reduced our equity exposure (maintained at 10% to 35% since last few months depending on client’s risk profile and the levels at which we started managing their portfolio) gradually over the last two years and limited it to only large-cap schemes. We stopped making a fresh allocation to mid/small cap schemes from mid-2017 and exited entirely by March/April 2018 due to excessively steep valuations. Entry/exit calls on IT sector has also worked quite well. In order to hedge equity exposure against rising global uncertainties and weakening domestic fundamentals, we allocated a decent portion of our client’s portfolio in gold funds over the last 1 year which has played out well so far. We suggested our readers to start looking at gold allocation in our blog written last year.

Despite the correction over the last one year, we are still not very comfortable with the price levels (across all market caps) as guided by our in-house valuation framework. Going ahead, we are patiently awaiting the comfortable price levels (vs. fair value) to gradually increase our equity exposure. When we would reach those levels is difficult to say but we have immense patience to hold on. Our focus has always remained on taking equity exposure at comfortable valuations with a margin of safety in mind. The strategy works in all market scenarios. Lower the price, higher is our comfort zone. We are hoping that we do not come to a situation of a severe market downturn. However, if it comes, we are ready.

Truemind Capital is a SEBI Registered Investment Management & Personal Finance Advisory platform. You can write to us at connect@truemindcapital.com or call us on 9999505324.

4 Comments

Very well articulated . Challenge is that investor thought process gets clouded by the sentiments in the market nd the fear of missing the bus of positive cycle 🙂

That’s true. One needs to be aware of the sentiment cycle to generate higher risk adjusted returns.

Very informative and well done!

Thank you for the feedback.